One of the best hidden hacks in building wealth through real estate many investors don’t know about are DSCR Loan cash-out refinances. While some people may know about cash-out refinances for tapping equity in their home, many people, including seasoned real estate investors, don’t know you can cash-out refinance a rental property too!

What are Cash-Out Refinance DSCR Loans?#

A cash-out refinance DSCR transaction type refers to situations where a borrower is taking out a loan on a rental property they already own. In a cash-out refinance, the subject property can either be owned free and clear (meaning no existing mortgage), or it can have an existing loan that would be paid off upon funding. DSCR Loans are a type of mortgage loan defined as a loan secured by residential real estate turnkey properties strictly used for a business purpose and underwritten primarily based on the property.

A refinance loan is considered to be “cash-out” typically when the cash-out proceeds you receive are in excess of $2,000 (this is generally the difference between the new loan amount and the old loan amount paid off, plus closing costs and escrows). If you receive less than $2,000 or even have to “bring money to the table” (sometimes called a “cash-in refinance”), this is generally called a “rate-term refinance.”

Cash-Out Refinances are a popular tool for all types of mortgages, including conventional loans, either owner-occupied or investment properties, and of course DSCR Loans, the most popular loan type for real estate investors. For investors utilizing the popular BRRRR Method, the refinance, or the third R in the acronym, is very important for success. Executing the refinance, ideally a cash-out refinance (though not necessary), of the BRRRR Strategy. In April 2023, when Fannie Mae decreed that there must be a 12-month “seasoning” requirement to do a conventional cash-out refinance, DSCR Cash-Out Refinances became the preferred option for BRRRR investors.

How to Cash-Out Refinance a Rental Property#

As you can imagine, the process begins by applying for a loan. The standard loan application process typically takes about 5-10 minutes. In addition to completing the application, you’ll also sign a document authorizing a credit report. The type of information required will vary depending on the loan type. For example, a conventional loan may ask for property details, income, and tax history. Investors applying for a DSCR Loan will face a more straightforward application. DSCR loans don’t require income or personal financials but may require LLC information and a detailed rent roll.

It’s important to note that cash-out refinance DSCR loans must be for a “business purpose.” The mortgaged property must be a rental property, meaning the borrower cannot live in it. This includes properties with multiple units. The cash-out proceeds must also be used for business purposes. This vague definition allows for various uses, but real estate reinvestment is the most common. Business purposes may include capitalizing a separate business or paying company taxes or debt. Personal uses, like paying personal taxes, vacations, or credit cards, are prohibited.

This requirement applies to the loan’s intention at origination. However, if extraordinary life changes occur, such as a personal emergency, leftover proceeds could be used for personal use.

What are the Tax Implications for a Rental Property Cash-Out Refinance?#

A big reason Cash-Out Refinances are so popular among investors is that it is an opportunity to access a large cash infusion without having to pay taxes on the amount. This is because since it is simply a new loan, it is not considered “income” and since you are not selling the property it is not a “realized gain.” This tax advantage makes cash-out refinancing a popular strategy among real estate investors for growing their rental portfolios.

DSCR Loans are very prevalent for real estate investors with long-term horizons and strategies to grow portfolios by adding properties to a portfolio over many years. Accessing equity in appreciating properties without having to subtract from your portfolio or having to pay taxes on any capital gains make cash-out refinances the top tool in the toolbox of many successful investors that achieve large and lucrative SFR portfolios.

What are Cash-Out Refinance DSCR Loan Interest Rates?#

Generally, DSCR Loans are around 0.75% to 1.00% higher in interest rate than conventional mortgage loans, although this can vary depending on multiple factors. Additionally, Cash-Out Refinances are often considered a little riskier for lenders than acquisition or Rate-Term Refinance transactions. This is due to a multitude of factors, but primarily because of historical performance data and uncertainty of value versus purchase transactions.

Nonetheless, the rates are not too much higher for Cash-Out Refinance DSCR Loans. Typically, the difference will be between only around 25 to 50 basis points (0.25% to 0.50%), but will vary among DSCR Lenders. Additionally, there are typically lower leverage (LTV) limits on cash-out refinances, generally with maximum LTVs 5% less than equivalent rate-term refinances. For example, if the lender’s maximum LTV for a rate-term refinance scenario is 80.0%, the maximum LTV for a cash-out refinance DSCR loan in this scenario would be 75.0%.

Should I do a Cash-Out Refinance on my Rental Property?#

While cash-out refinances offer significant benefits, there are multiple factors to consider. These include access to capital without a taxable event and potential tax benefits. A large factor is current market interest rates and the rates and terms you qualify for at the time of refinance application. In times of dropping interest rates, cash-out refinances become very popular. Borrowers get cash in hand and can lower their loan rate by paying off the old, higher-rate loan.

In times of elevated rates, the new loan in the cash-out refinance can have a higher rate. This could lead to a large increase in your mortgage payment, reducing your monthly cash flow. Even if your rate stays the same or decreases, a higher mortgage payment may occur due to a larger loan balance.

The decision to do a cash-out refinance is not always simple. It comes down to your current situation and real estate investing game plan. The primary factor is the planned usage for the cash-out proceeds. If any downsides from higher rates or payments are outweighed by a new investment opportunity, the cash-out refinance makes sense. Always run the numbers and do a scenario analysis before considering cash-out refinances. Monitor market movement with a trusted lending partner.

Easy Street Capital Cash-Out Refinance DSCR Loans#

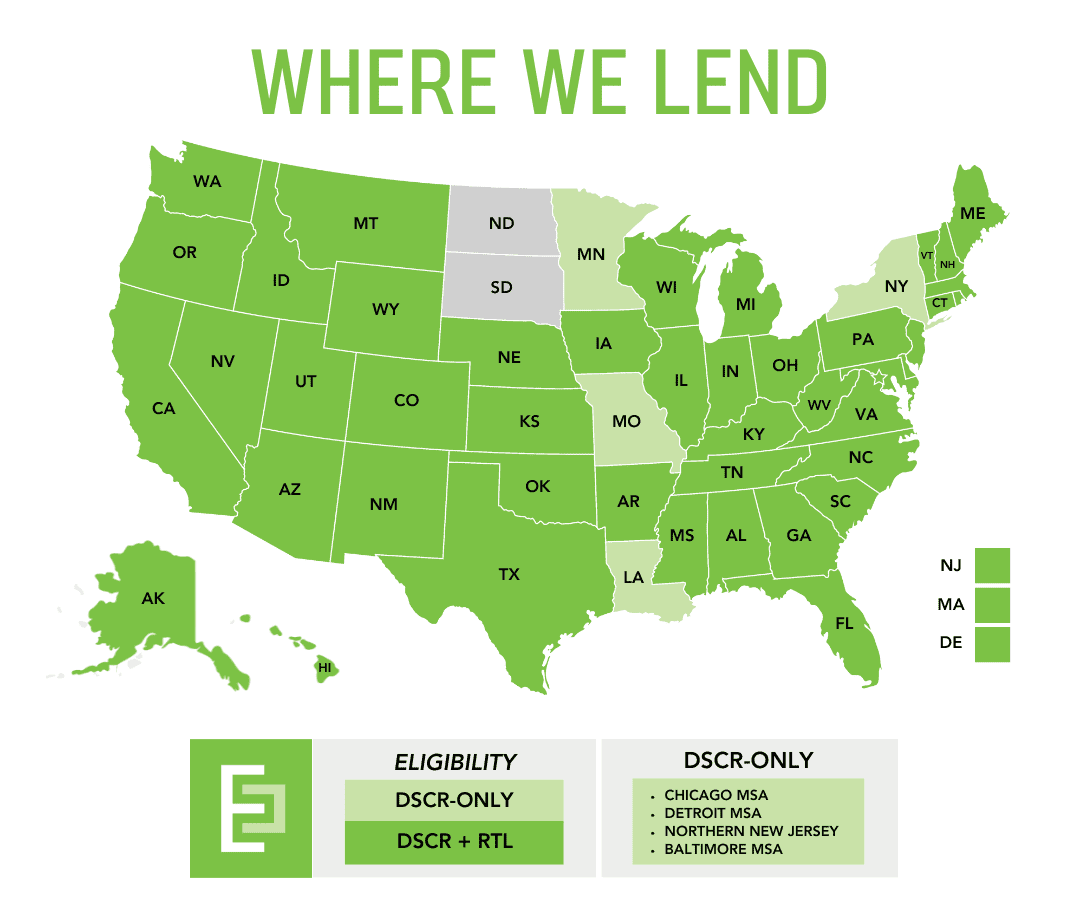

Easy Street Capital is one of the nation’s top DSCR Lenders and offers a wide variety of cash-out refinance DSCR Loans for rental properties in 48 states. Here are some of the common questions we receive regarding Cash-Out Refinances:

What is the maximum LTV for a Cash-Out Refinance DSCR Loan?#

Easy Street Capital’s maximum LTV (Loan to Value Ratio) for cash-out refinances is 75%. Generally, this is the maximum LTV for cash-out refinances among DSCR lenders, although sometimes 80% LTV will be offered. Its generally advised to be careful when looking at 80% LTV cash-out refinance options, as the rates and fees are typically going to be exorbitant to account for the outsized risk.

What is the seasoning period for Cash-Out Refinance DSCR Loans from Easy Street Capital?#

In the context of DSCR loans, seasoning period refers to the amount of months a property has been owned. Easy Street Capital has no minimum seasoning period for cash-out refinance DSCR loans. However, the value used to qualify the loan and the LTV ratio are important factors. For loans with a seasoning period between 0 and 3 months, Easy Street Capital will provide cash-out refinance DSCR loans. You must use the lower of the third-party appraised value and your cost basis (purchase price plus documented renovation costs).

Easy Street Capital offers Cash-Out Refinance DSCR Loans with as little as three months seasoning. The appraised value is used if it’s higher than the costs. You must have a qualifying credit score of 700 or better. The loan amount must be equal to or less than the cost basis. Cash-Out Refinance DSCR Loans with seasoning between 3-6 months will be limited to 70% LTV. This applies if the two requirements are met.

For cash-out refinance DSCR loans with six months or greater seasoning, Easy Street Capital has no seasoning restrictions. The third-party appraisal will be used every time for valuation purposes.

What is the minimum DSCR Ratio for a Cash-Out Refinance DSCR Loan?#

Easy Street Capital has no minimum DSCR ratio for cash-out refinance DSCR Loans! This means borrowers can qualify for a cash-out refinance on their rental property with an underwritten DSCR ratio of less than 0.75x! In these cases, the LTV can even be as high as 70%, just 5% lower than our overall maximum!

Does my rental property need to be leased for a Cash-Out Refinance DSCR Loan?#

Easy Street Capital is the leading DSCR lender for short-term rentals. It has pioneered cash-out refinances for ‘AirBnBRRRR’ investors. ‘AirBnBRRRR’ combines Airbnb investing with the BRRRR method. An integral part of success with this strategy is executing a cash-out refinance without a long-term lease. Instead, investors list the property on short-term rental platforms like Airbnb. Easy Street Capital is a rare DSCR lender that offers cash-out refinances for short-term rentals. We don’t require 12 months of operating history. We only need a listing and one completed or in-progress booking.

For rental properties that are vacant and not used as short-term rentals, cash-out refinance DSCR loans are generally unavailable. However, exceptions can apply from time to time. Some examples include refinancing large ‘Build to Rent’ portfolios or multi-unit properties with one or two vacant units. Consult your loan specialist to discuss whether a vacant rental property cash-out refinance qualifies. We generally recommend leasing the property before closing your cash-out refinance DSCR loan if it’s not used as a short-term rental.

What is the minimum Credit Score for a Cash-Out Refinance DSCR Loan?#

The minimum qualifying credit score or (FICO score) for a Cash-Out Refinance DSCR Loan with Easy Street Capital is 640. However, to get the best rates and access to the most programs and options, 660 is the minimum score to aim for cash-out refinances with Easy Street.

Ready To Get Started?#

#

Thinking about a Cash-Out Refinance on one of your rental properties? Or would you like to learn more about Easy Street’s DSCR Loans for future investing? Request a Term Sheet today. You can also book a call with one of our Cash-Out Refinance loan specialists.

Disclaimer: The information provided in this article is not intended as financial or legal advice of any kind. Regulations regarding short-term rentals are subject to change and all investments are subject to risk. Information included in this article may contain information that has not been verified by licensed attorneys and should be subject to independent verification. Readers are advised to consult with qualified legal or financial professionals prior to investing in real estate investment properties.